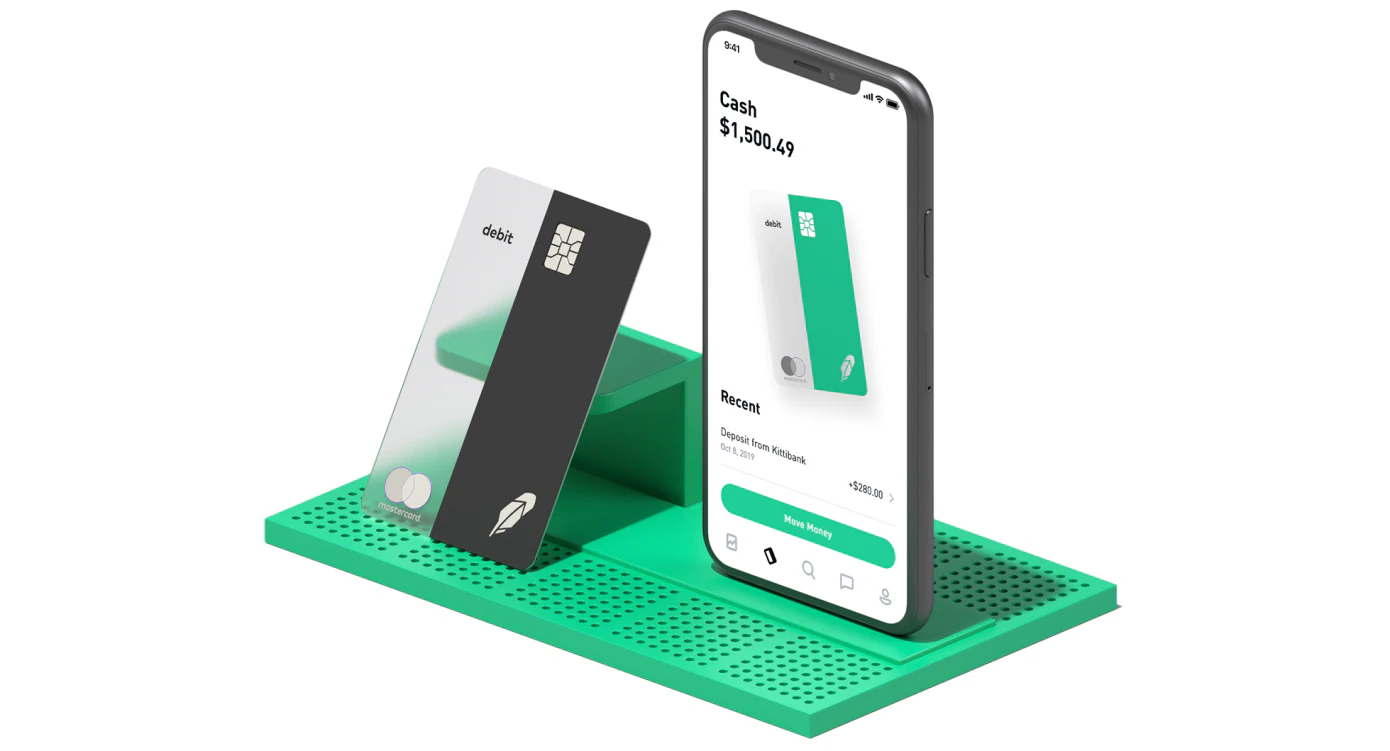

Trump Accounts

Build long-term financial security for your child

Trump Accounts help eligible American children begin building long-term financial growth from an early age. Eligible children born between 2025–2028 can qualify for an initial $1,000 U.S. Treasury contribution beginning July 4, 2026. The account features a pilot program contribution of $1,000 for children born between Jan. 1, 2025, and Dec. 31, 2028, and who are U.S. citizens with a valid Social Security number.

AI Analysis

Trump Accounts provide eligible U.S. children born 2025-2028 with a $1,000 initial U.S. Treasury contribution to build long-term financial security through investing. Core features include government-seeded accounts for early wealth accumulation, focused on kids, investing, and parenting. It solves parents' pain points of insufficient early savings and high future costs for education/living. Unique selling point is the automatic Treasury seed money starting July 4, 2026, for qualifying citizens with SSN, offering a valuable head start on compounded growth and financial independence.

The timing is favorable for 2025-2026 with emphasis on family support policies, rising awareness of early childhood investing, and economic pressures increasing demand for savings tools. It aligns with potential pro-family economic initiatives and technology maturity in fintech for account management. However, success hinges on policy approval and economic conditions. Rating: Excellent Timing.

Overall feasibility is Medium. Technical setup for accounts is straightforward using existing fintech infrastructure, but faces high compliance/regulatory risks due to government involvement, Treasury contributions, and eligibility verification. Development and operation costs could be significant for scaling to millions; political risks affect rollout. Scalability is high post-launch but team fit depends on governmental execution. Rating: Medium.

Main target segments: American parents (ages 20-45) of children born 2025-2028, especially middle-income families interested in long-term investing; U.S.-wide geographic distribution. Estimated TAM for child investment/savings products exceeds $50B; SAM for government-eligible newborns ~3.5M births/year or 14M over period; SOM depends on adoption. Core pain points: inadequate savings for rising education/child-rearing costs. Willingness to pay: High for additional contributions or related advisory services.

Competition level: Medium. Direct competitors: 1. 529 College Savings Plans (savingforcollege.com), 2. Acorns Early (acorns.com/early), 3. Greenlight Invest (greenlight.com), 4. Vanguard UTMA/UGMA accounts (vanguard.com), 5. State Baby Bonds (e.g., Connecticut's program). Advantages: Unique $1000 government seed, patriotic branding, simplicity for eligible births. Disadvantages: Restricted eligibility (specific birth years only), potential limits on withdrawals/use, less flexibility than private fintech solutions, and dependency on federal implementation vs. ongoing commercial innovation.

Upgrade Pro to unlock full AI analysis

Similar Products

Robinhood Agentic Trading

Let your agent trade

▲ 148 votes

Metal

AI-driven operating system for raising venture rounds

▲ 124 votes

Orus

Claude for investing in perpetuals

▲ 121 votes

Robinhood Agentic Trading

Let your agent trade

▲ 0 votes

Robinhood Agentic Trading

Let your agent trade

▲ 0 votes

WeLiveLife

Elderly Care At the Comfort of Your Home

▲ 0 votes